If you’ve been searching for ways to buy a home in California, chances are you’ve seen headlines, social posts, and TikToks talking about California Dream For All. It’s one of the most discussed homebuyer assistance programs in the state, and for good reason.

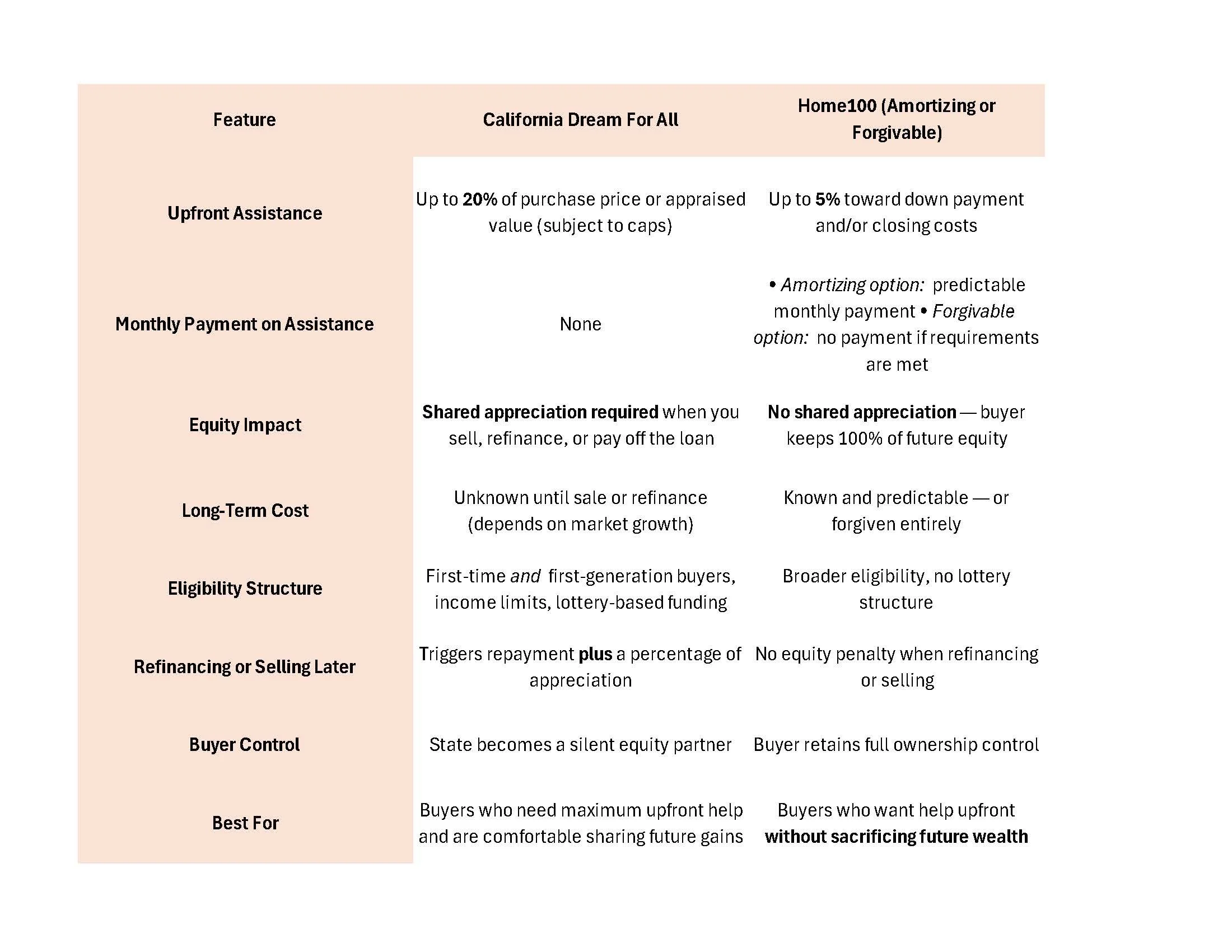

The program offers up to 20% of the purchase price or appraised value as down payment assistance. That’s a big number, especially in a market where saving for a down payment can feel impossible.

But while the California Dream For All Shared Appreciation Loan can help buyers get into a home sooner, it also comes with long-term trade-offs that many buyers don’t fully understand until later.

That’s why it’s important to compare it against other programs, including Home100, a down payment assistance option that works very differently and is available nationwide, not just in California.

This guide breaks down:

How California Dream For All really works

What “shared appreciation” actually means for your future wealth

How Home100 compares (amortizing and forgivable options)

Why many buyers find Home100 to be the better long-term choice

What Is California Dream For All?

California Dream For All is a shared appreciation loan program created to help eligible homebuyers with their down payment.

Here’s how it works in simple terms:

The program provides up to 20% of the purchase price or appraised value

The loan has no monthly payment

Instead of monthly payments, repayment happens when you:

Sell the home

Refinance

Or pay off the first mortgage

At that time, you repay:

The original assistance amount plus

A percentage of the home’s appreciation

In other words, the state becomes a silent equity partner in your home.

Why California Dream For All Is So Popular

There’s a reason California Dream For All gets so much attention:

It dramatically reduces the upfront cash needed to buy

Buyers can qualify with little money out of pocket

There’s no monthly payment on the assistance

It helps buyers compete in higher-priced markets

For buyers who are otherwise locked out of homeownership, this can feel like a lifeline.

But the structure matters, especially over time.

The Trade-Off: What Shared Appreciation Really Means

The key feature of California Dream For All, shared appreciation, is also its biggest long-term cost.

When your home increases in value (which is historically common in California), the program requires you to share a portion of that growth when you sell or refinance.

That means:

The more your home appreciates, the more you owe

The cost isn’t predictable at the beginning

Refinancing later can trigger a large repayment

Your equity is partially spoken for before you even build it

For buyers who plan to stay long-term, refinance, or build generational wealth, this can significantly reduce the financial upside of homeownership.

Introducing Home100: A Different Kind of Assistance

Home100 takes a very different approach.

Rather than shared equity, Home100 provides down payment and/or closing cost assistance through a second lien — with no appreciation sharing.

There are two primary Home100 structures:

1. Amortizing Home100

Assistance is repaid gradually over time

Payments are predictable and transparent

Equity belongs fully to the homeowner

2. Forgivable Home100

Assistance may be forgiven after meeting occupancy or time requirements

No shared appreciation

No repayment if conditions are satisfied

And most importantly:

👉 Home100 is available nationwide, not just in California.

California Dream For All vs Home100: The Real Difference

Both programs help buyers get into homes.

They just answer very different questions.

Dream For All: “How can I buy today with the least money upfront?”

Home100: “How can I buy smart and keep what I build over time?”

Let’s break that down.

Why Home100 May Be the Better Option for Buyers

1. You Keep 100% of Your Home’s Appreciation

With California Dream For All, appreciation is shared.

With Home100, it’s not.

Whether you choose the amortizing or forgivable option:

The equity you build belongs entirely to you

There’s no state or agency claiming a portion later

Refinancing doesn’t trigger an appreciation payout

For buyers thinking long-term, this matters more than many realize.

2. Predictable Costs Instead of Uncertain Future Repayment

Dream For All’s cost depends on:

Market performance

Timing of sale or refinance

How much appreciation occurs

That makes future planning difficult.

Home100 offers:

Known monthly payments (amortizing)

Or potential full forgiveness (forgivable option)

No surprise equity calculations later

Predictability reduces stress — and risk.

3. Home100 Isn’t Limited by California-Only Rules

California Dream For All has:

Income limits

First-time and first-generation buyer requirements

Limited funding windows

Lottery-based selection

Home100:

Is offered nationwide

Has broader eligibility

Can be used by buyers relocating, moving out of state, or buying again

Doesn’t rely on random funding cycles

That flexibility is especially valuable in today’s mobile workforce.

Who Should Consider California Dream For All?

Dream For All can make sense for buyers who:

Need the maximum possible upfront assistance

Don’t expect significant appreciation

Plan to stay in the home without refinancing

Understand and accept shared equity

It’s not wrong, but it’s specific.

Who Often Benefits More from Home100?

Home100 tends to be better for buyers who:

Want to build and keep long-term equity

Plan to refinance in the future

Value predictability

May move or buy in another state later

Want assistance without long-term strings attached

Homeownership Is About More Than Getting In

Buying a home isn’t just about crossing the finish line.

It’s about:

What you keep

What you control

And what flexibility you have later

That’s where the difference between these programs really shows up.

Q&A: California Dream For All — Buyer Questions Answered

Below are some of the most searched questions about California Dream For All, with honest, buyer-focused answers, and how Home100 compares.

Is California Dream For All really free money?

No. It’s a loan with shared appreciation.

Home100, especially the forgivable option, can actually result in true forgiveness without shared equity, making it a better long-term value for many buyers.

Do you have to pay back California Dream For All?

Yes, when you sell, refinance, or pay off your mortgage.

With Home100 forgivable options, repayment may not be required at all if conditions are met.

Does California Dream For All take part of my equity?

Yes. That’s how shared appreciation works.

Home100 allows buyers to keep 100% of their equity growth.

Can I refinance with California Dream For All?

You can, but refinancing triggers repayment and appreciation sharing.

Home100 does not penalize refinancing with equity sharing.

Is California Dream For All only for first-time buyers?

It’s limited to first-time and first-generation buyers and subject to funding availability.

Home100 is available to a broader range of buyers nationwide.

What happens if home values rise significantly?

With Dream For All, you owe more.

With Home100, appreciation benefits only you.

Is Home100 available outside California?

Yes.

That’s one of its biggest advantages, it works nationwide, making it ideal for relocations or future purchases.

Final Thoughts: Choose the Program That Fits Your Future

California Dream For All has opened doors for many buyers, and it deserves credit for that.

But homeownership isn’t just about buying today.

It’s about what happens five, ten, or twenty years from now.

For buyers who want:

Control

Predictability

Equity retention

Nationwide flexibility

Home100 often provides a stronger foundation.

At Best Option Mortgage, the goal isn’t to push a single program, it’s to help buyers choose the strategy that actually supports their future.

Ready to Compare Your Options?

Every buyer’s situation is different.

Comparing programs before writing an offer can save you tens — or hundreds — of thousands of dollars over time.

——

Best Option Mortgage is a DBA of ML Mortgage Corp. ML Mortgage Corp. is a state-licensed mortgage lender, NMLS ID #362312. Licensed by the California Department of Financial Protection and Innovation under the Finance Lenders Law, License #60DB069831. For licenses in other states, visit www.mlmortgage.net. To verify licensing, visit www.nmlsconsumeraccess.org. All loans are subject to credit approval and acceptable collateral. Terms, rates, and programs are subject to change without notice and may not be available in all states. This is not a commitment to lend. Additional restrictions may apply. Not all borrowers will qualify. Equal Housing Opportunity © ML Mortgage Corp. All rights reserved. Updated 2026.